Net Lease Market Research Report Date November 1, 2016

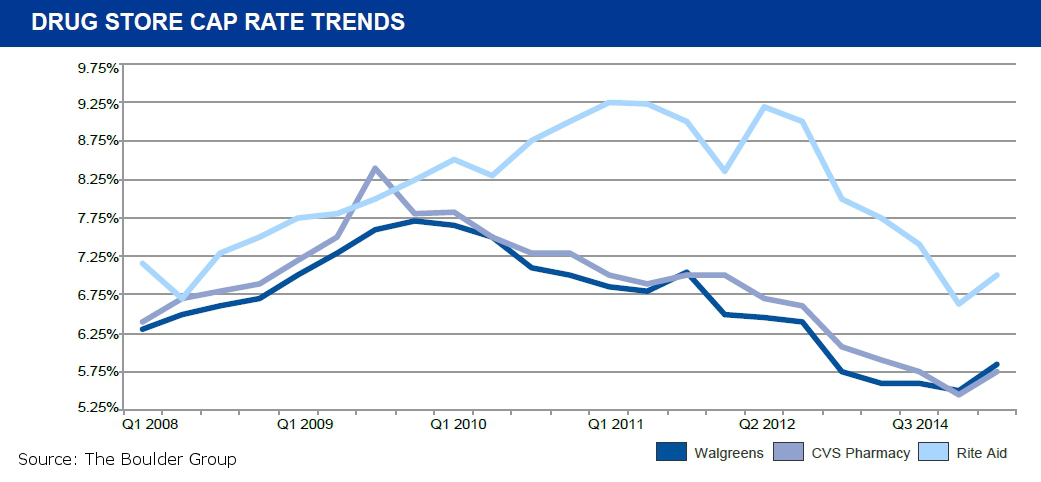

Our new net lease market research shows cap rates for single tenant CVS, Rite Aid and Walgreens properties all increased significantly in the third quarter of 2016. Cap rates for the net lease drug store sector increased by 33 basis points to a 5.96% cap rate when compared to the prior year. Rite Aid and Walgreens cap rates experienced the largest increase by 30 and 37 basis points each due to the investor concern of store closures with the potential Rite Aid acquisition by Walgreens. In the same timeframe, CVS cap rates increased by 25 basis points.

Transaction volume in drug store sector has been slowed by investor trepidation due to the uncertainty of the potential Walgreens and Rite Aid merger. However, investment sales activity has been concentrated with drug store assets in core markets with strong sales performance. The concern from the merger has caused the cap rate premiums associated with the drug store sector to decrease. In the third quarter of 2016, the spread between the overall net lease retail market and the drug store sector compressed to 14 basis points. This spread has historically been greater and in the past three years the spread ranged from 75 to 100 basis points.

The supply of drug store assets decreased when compared to the prior year by 23.2%. Not only did the availability of drug store assets decrease, closed transaction volume for drug stores decreased by 19.2% when comparing the first three quarters of 2015 and 2016. Rite Aid assets experienced the sharpest decline with 26% less transaction volume during the same time period. Furthermore, the supply of long term leased (20+ years) assets decreased significantly across the sector due to lack of new store development.

Transaction velocity for the remainder of 2016 in the net lease drug store sector should remain at a similar pace to the first three quarters of 2016 as uncertainty remains due to the potential Walgreens and Rite Aid merger. However, drug store assets with strong sales performance in top tier markets will garner demand from investors who have preference for the strong credit profiles and residual real estate locations that these drugstore assets provide. Private investors will continue to be the primary buyer of these assets.

Back